Good morning, Construction Pros. Penn Station finally has a builder, copper is running hot with a 50% tariff still attached, and April starts suggest the work picture is wider than it looked in March.

- $8 billion, one team: USDOT and Amtrak picked a master developer for the Penn Station rebuild and the job is considerably harder than the dollar figure suggests.

- Copper at $13,570/MT: LME spot is up 4.7% month over month and the Section 232 tariff is still active at 50%, which means electrical bids need sharper buyout language than they did six months ago.

- April starts broadened out: Nonresidential building jumped 18.6% and more project types contributed, not just the usual hyperscale suspects.

Know someone who would like this? Pass it on.

📊 MARKET PULSE

| LABOR INDICATORS | |

|

CONSTRUCTION JOB OPENINGS

224K

+23K MoM, down 54K YoY

|

CONSTRUCTION HIRING RATE

3.7%

Near historical low

|

|

CONSTRUCTION QUIT RATE

1.7%

Below 2019 baseline

|

CONSTR. UNEMPLOYMENT RATE

3.8%

Apr 2026, down from 6.7% in Mar

|

| MATERIALS & COSTS | |

|

COPPER (LME SPOT)

$13,570

Per MT | +4.7% MoM | 50% tariff active

|

STEEL, DOMESTIC MILL

$1,155

Per MT | +0.2% | Sec. 232 at 50%

|

|

NONRES. INPUT PRICES

+7.4%

YoY | +6.2% YTD (since Jan)

|

RETAIL DIESEL (WILD CARD)

$5.596

Per gal | +61% YoY

|

LABOR PULSE

This is neither a buyer's nor seller's market for construction labor right now, it is a frozen one. Sector unemployment dropped hard from 6.7% to 3.8% as spring work ramped, but hiring rates and quit rates tell a different story: contractors are filling holes, not expanding, and workers are staying put rather than shopping offers. For a foreman staffing a new job, that means the skilled pool is not flooded but it is not mobile either. You can hire, but count on it taking longer and costing more in specialized trades than the overall numbers suggest.

THE TAKEAWAY

Nonresidential input costs are up 6.2% since January alone, and copper is carrying a 50% tariff on top of spot-price gains. Any bid priced on winter 2025 assumptions is already underwater before the first delivery. Add escalation riders with indexed benchmarks, and build tariff pass-through language into copper-heavy scopes before you sign.

🏗 THE BIG MOVES

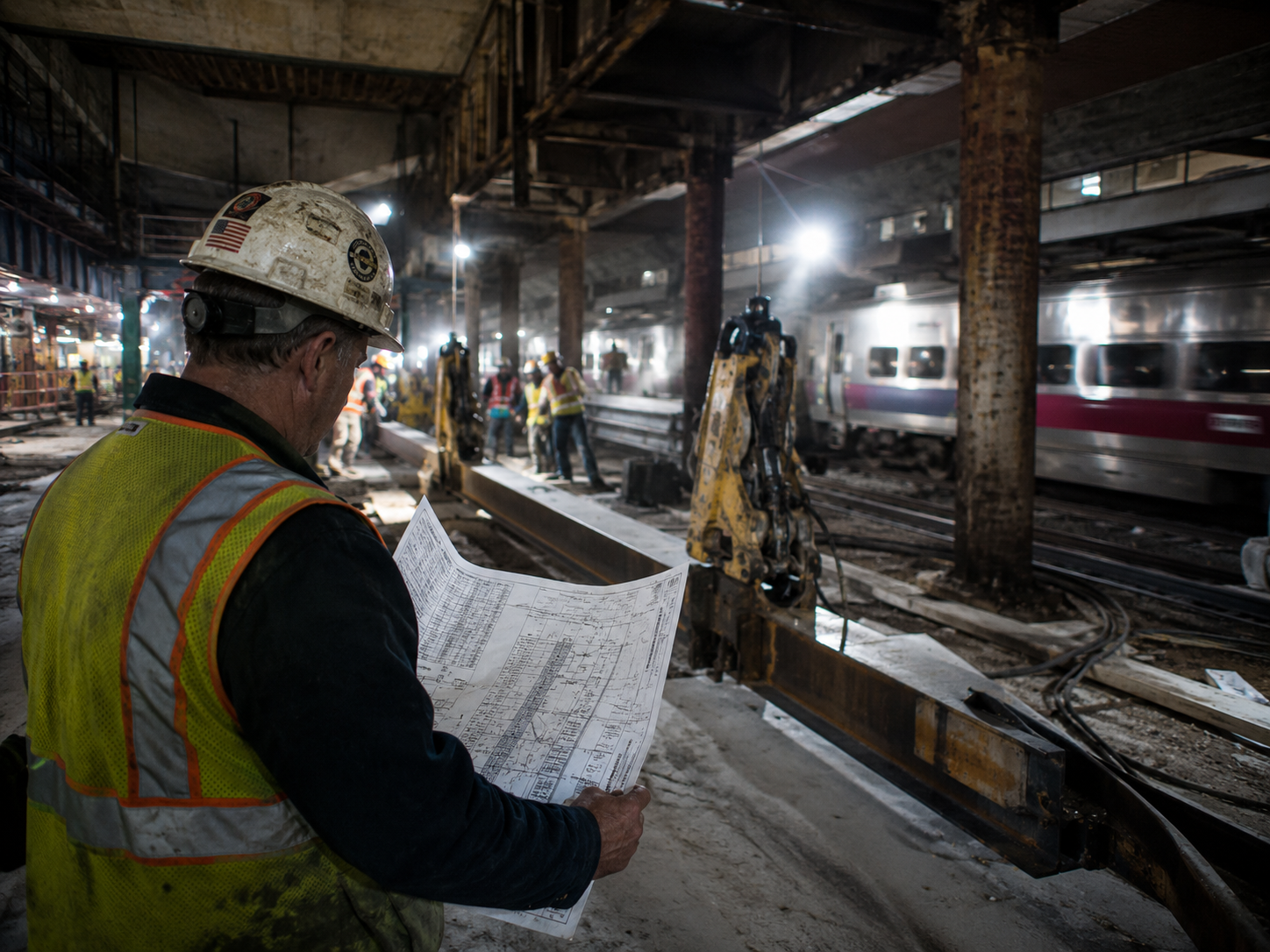

Halmar-Skanska Team Named Master Developer for $8B Penn Station Rebuild

USDOT and Amtrak announced on May 20 that Penn Transformation Partners, a joint venture of Halmar International and Skanska, was selected as master developer for the $8 billion New York Penn Station renovation, with USDOT adding $200 million immediately to keep the program on track for a 2027 groundbreaking. The project involves active-rail construction, a single-level concourse conversion, and intricate phased staging directly beneath Madison Square Garden, making it one of the more logistically difficult builds in the current U.S. pipeline regardless of its size. Structural, civil, MEP, life-safety, and transit-systems trades face real complexity here: outage windows, occupied-facility constraints, and transit-safety compliance will separate experienced crews from everyone else.

IBM Launches $2B Anderon Quantum Chip Plant at Albany NanoTech Complex

IBM will receive a $1 billion federal grant and commit another $1 billion of its own capital to build Anderon, a standalone quantum-computing chip manufacturing company, at the Albany NanoTech campus in New York, with GlobalFoundries receiving an additional $375 million for related quantum programs. The headline says "quantum," but the field reality is a precision industrial buildout: clean rooms, process piping, vibration-controlled slabs, high-capacity electrical distribution, controls integration, and ultra-pure MEP systems that leave little tolerance for shortcuts. Electrical, mechanical, controls, and specialty concrete crews with prior semiconductor or advanced-manufacturing experience are the primary labor target; a GC had not been publicly announced as of publication.

Stream Data Centers Proposes $20B AI Campus in Genesee County, New York

Texas-based Stream Data Centers is pursuing a $20 billion AI campus in Genesee County, New York, with roughly $1.4 billion in proposed tax incentives, part of a wider wave of data-center proposals currently forcing public debate over grid capacity, community concessions, and permanent job counts in upstate New York. If it advances, construction demand would run deep across civil, earthwork, concrete, structural steel, electrical, medium-voltage, mechanical cooling, and utility interconnection crews for years. The project is still at a politically contested stage: grid politics and incentive negotiations remain unresolved, and the timeline has not been publicly stated.

🔦 PROJECT SPOTLIGHT

CIVIL STRUCTURAL MEPNew York Penn Station Renovation, New York City

The Penn Station renovation is an $8 billion federally backed program to build a new passenger station in Manhattan while keeping one of the busiest rail hubs in the Western Hemisphere fully operational throughout construction, with the Halmar-Skanska Penn Transformation Partners team now named as master developer and targeting a 2027 groundbreaking.

ENR reports that the team inherits active-rail construction, a single-level concourse conversion, and layered staging constraints directly beneath Madison Square Garden, all while the station processes roughly 600,000 daily passengers. For trades, this means the work envelope is extraordinarily tight: demolition and concrete crews must operate within rail service windows, structural tie-ins need precise sequencing around live track, and MEP and life-safety crews face transit-grade integration requirements that are categorically different from a standard commercial build.

WHY IT MATTERS

Penn Station is a template for a broader construction reality: the U.S. is increasingly replacing critical transportation and infrastructure assets in place rather than shutting them down first, and that logic is showing up in airports, rail corridors, hospitals, and water systems across the country. Contractors who know how to phase work around live operations are not just more useful on jobs like this one; they are building the credential that puts them in the room on the next one. If you have night-shift or outage-window experience, this is worth tracking as the delivery phase ramps.

The master developer selection is complete and preconstruction is advancing; the program is targeting groundbreaking on a new station in 2027, with the full build expected to run multiple years through one of the most complicated urban construction envelopes in the country.

⚡ QUICK HITS

Oregon DOT plans 1,000-plus layoffs. A $242 million funding shortfall has forced the Oregon Department of Transportation to plan significant workforce reductions and halt planned highway repair programs pending a public vote on a transportation funding bill. Heavy equipment operators and civil laborers in Oregon face direct job risk, and the regional public works bidding pipeline is effectively frozen until the vote resolves.

Cal/OSHA indoor heat enforcement is live. California regulators have launched active compliance sweeps on commercial and industrial job sites to enforce indoor heat illness prevention rules as summer temperatures climb. Any enclosed work environment hitting 82 degrees Fahrenheit triggers mandatory employer provisions for fresh water, shaded cool-down zones, and heat training, with stricter monitoring required at 87 degrees.

California kills stay-or-pay training contracts. Assembly Bill 692 took full effect this month, making it unlawful for contractors to require workers to sign training repayment agreements that can trap them in low-wage positions under threat of debt collection. Government-registered union apprenticeship programs retain a specific exception, preserving that funding model while eliminating the predatory non-union version.

OpenAI shelves Stargate UK over energy costs. The company officially paused its multi-billion-pound UK AI data center development, citing high energy costs and slow utility-level approvals, redirecting near-term capacity investment to Narvik, Norway. The cancellation is a direct reminder that speculative technology builds live or die on grid access, and preconstruction pipelines for major GCs are the first thing to dry up when utility infrastructure stalls.

April construction starts hit a $1.33T annual rate. Dodge reports total starts jumped 9.0% month over month, with commercial starts surging 41.4%, led by offices and data centers, and nonresidential building alone reaching a $550 billion annualized pace. That breadth means work is spreading beyond the usual megaproject suspects, opening opportunities across more trades and more regions.

🔢 ONE NUMBER

Year-over-year increase in nonresidential construction input prices through April 2026, per ABC's analysis of BLS PPI data, with costs up 6.2% in just the first four months of the year.

🔧 THE TOOL

With copper at $13,570/MT on the LME and a 50% Section 232 tariff still running on covered copper articles, electrical-heavy bids need more than a general escalation clause. What actually protects you is a copper escalation rider built around a specific benchmark date: on the day you submit, document the LME official cash price or the exact supplier quote you priced to, and state it in the contract language. From there, any movement above an agreed threshold before material release becomes a documented change in contract value, not a margin-eating surprise you absorb.

Add a second sentence that separates tariff exposure from commodity price risk: write it so that any new or modified Section 232 duties, customs treatment, or tariff application to covered copper articles after your bid date are owner pass-throughs with a 10-day notification window, not subcontractor risk. The notification requirement is important, it forces the conversation before delivery, not after. This is directly relevant this week because the April 6 proclamation extended Section 232 duties to the full customs value of covered copper articles, which is a materially broader base than prior guidance, and the change is close enough to current bids that some subs are carrying risk they never priced.

📚 FURTHER READING

ENR: Halmar, Skanska Advance Penn Station Rebuild as Delivery Phase Begins - The best source for build-specific detail on active-rail work, concourse conversion, and phasing constraints. (Paywall risk noted below.)

Construction Dive: Construction starts jumped in April as more project types broke ground - Essential macro read for any sub trying to understand where the work pipeline is widening beyond hyperscale.

Construction Dive: Construction prices 'surged' in April, up 6.2% year to date - Details how tariff-impacted metals and diesel are compressing contractor margins heading into summer bid season.

Penn has a team, copper has a tariff, and April starts say the work is real across more project types than this time last month. Is the broader start mix showing up in your market, or are things still concentrated in one or two sectors? Hit reply and tell us. 🏗

Know someone who would like this? Pass it on.